Authored by Seaborn Hall, originally posted at Advisor Perspectives,

My previous article, “How likely is hyperinflation in the US? Part One,” covered hyperinflation's history, process, effects, definition, types and causes, as well as how to measure its emergence in nations using casual symptoms. Part Two answers the questions of how to gauge the likelihood of hyperinflation in the United States, what the emerging dangers are, how it might happen here and how to prepare if it does.

As stated in Part One, because there are so many conflicting or just different views among analysts relative to hyperinflation, it is difficult for the average advisor or person investing for retirement – or just self-preservation – to know what to believe and how to act. Many of the warnings related to hyperinflation sound like Chicken Little's cry that the sky is falling.

In the midst of the alarmism and confusion, these articles sift through the best resources available, including Bank for International Settlements (BIS), International Monetary Fund (IMF), Cato Institute and Fed papers to provide some clarity.

Measuring hyperinflation in the U.S.A.

The U.S. has come just short of hyperinflation twice before: once during the Revolutionary War and the second time, in March 1864, towards the end of the Civil War. The wars created high debt and supply disruptions within the continental states, congruent with fast acting hyperinflation, as explained in Part One.

The U.S. has geographic advantages. It has natural supply routes made up of rivers, natural ports and inter-coastal waterways connected by a sophisticated rail and interstate system. It is protected by the natural boundaries of oceans, mountains and friendly bordering states. It is also not dependent on one export, like oil. These geographical and man-enhanced attributes temper any economic trend towards hyperinflation in the modern U.S.

As previously noted, hyperinflation may be expected when there is persistent monetization and when the currency exchange premium – the premium the most-used foreign currency commands over the native currency – rises above 50%. This later sign typically occurs during a period of high inflation and up to three years before hyperinflation appears. This period may or may not include a currency crisis, which is distinct from, and can be an initial phase of, high inflation or hyperinflation. More broadly, the dangers of hyperinflation are measured by casual symptoms. These include fiscal, monetary and political causes and symptoms.

As to fiscal symptoms in the U.S., according to a recent JP Morgan (JPM) presentation, net U.S. debt is presently around 75% of GDP, high, but non-critical. Foreign officials hold 35% of this debt; the Fed holds 16 percent. Both are significant, but not excessive. And, as Prasad and Ye note, debt cements the U.S. dollar role as global reserve; that is, as long as it is not unsustainable, and interest is a manageable piece of the total budget (chart, below).

On this front, the U.S. does not have enough reserves to cover its short-term debt, but the Guidotti-Greenspan rule may not apply to Advanced Economies. And, as long as 10-year yields, currently about 2.35%, stay below 7% global bond investors tend not to panic, especially when the U.S. is the best of a bad lot.

Deficits-to-expenditures is marginal at about 18%. According to the Wall Street Journal, the deficit has decreased to only 3% of GDP in 2014. The deficit was $1.4 trillion six years ago and the Congressional Budget Office (CBO) projects it to be just $486 billion this year. But, it is expected to increase in 2016 and according to The Heritage Foundation could be worrisome again by 2021.

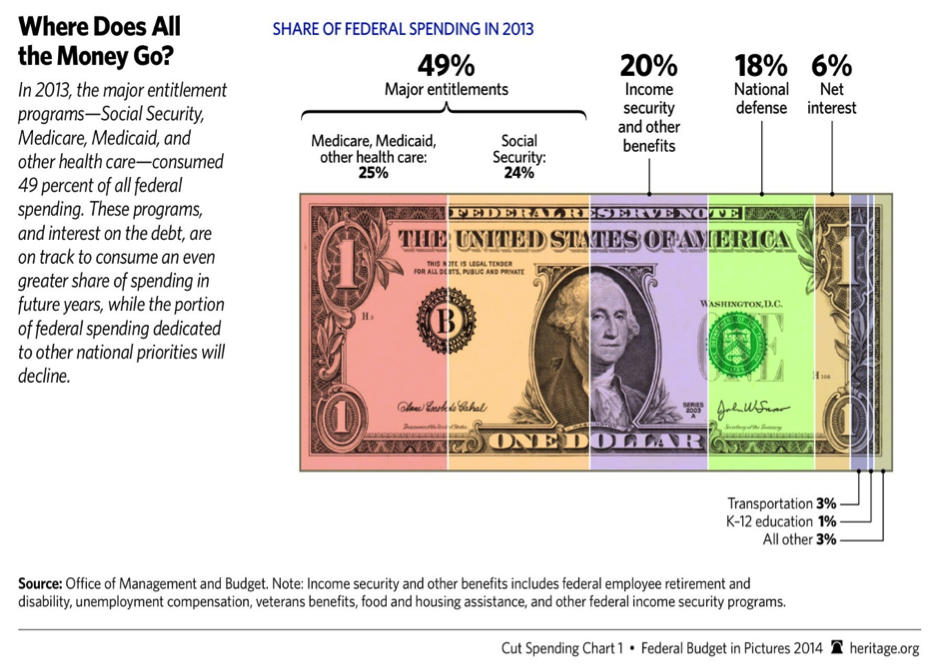

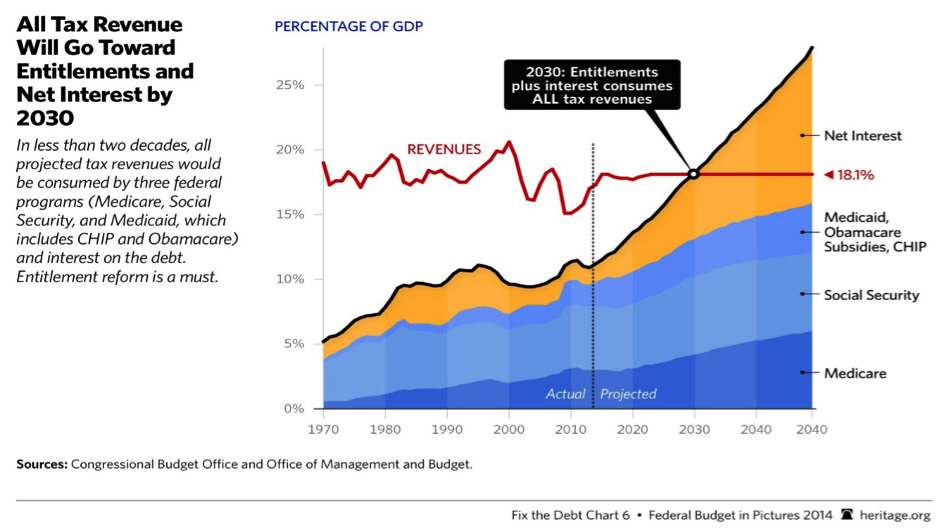

Also on the down side, according to Heritage, net U.S. debt, above, will reach 100% of GDP, a dangerous level, around 2028. At $18.2 trillion, total federal debt is already 102.5% of GDP. But most analysts feel that net debt (total minus intra-governmental debt) is the more critical measure. By 2024, mandatory expenditures, or entitlements plus interest on the debt, will be 75% of revenues. By 2030 they will consume revenues (chart, below).

As to monetary symptoms, Federal Reserve liabilities are also high, about $4.4 trillion. According to Guggenheim, the Federal Reserve's debt/equity ratio was 51:1 in July 2012, more than double 2008, and almost double commercial institutions that failed. And Fed Assets as a percentage of GDP have more than doubled since 2007. But central banks are judged differently, as Japan's experience implies, thus far at least. John Cochrane, a professor of finance at the University of Chicago, points out more specifically that Fed reserves do not lead to hyperinflation. It is also important to understand that printing money or QE is not necessarily the same as monetizing the debt.

In most cases, central banks control interest rates and reserves through government security and foreign currency purchases. To create money, a central bank purchases securities when it digitally credits the accounts of dealers with whom it does business. These dealer banks, like JP Morgan, are immediately richer. In some cases they park the money with the Fed, earning interest; in others, they invest it, some in riskier ways, like derivatives. For money velocity to increase they must actually loan it, which, according to Hanke, few currently do. This is partially due to increased federal regulations, like Dodd-Frank, instituted since the GFC, that place strict restrictions on lending activities.

Monetizing is when the central bank buys government securities directly from the Treasury to fund existing or, unplanned debt, as in the case of Zimbabwe or Japan at present (see Part One). An independent central bank firmly resists such pressure from the political power. The danger, of course, is that this distinction becomes unclear.

And, as a 2008 IMF report on the Fed stated, "Compared with its posture during the Great Depression, the Fed today is taking considerably more risk and the scope for possible profit and loss outcomes is much greater." The report also points out that the Fed's ability to make a profit during every year of the Great Depression era was largely due to its accumulation of gold. This is a far cry from the make-up of the Fed's burgeoning balance sheet today.

Another emerging hyperinflation danger is in the area of political management relative to economic health. The Obama administration has less business experience than previous administrations (chart above). Surveys also show that the American people see themselves as more divided than at any time in history (below), and other studies show that the political center is shrinking. Political mismanagement that suddenly increases the debt and social tensions could lead to a crisis that results in high inflation.

Years ago, R. E. McMaster, author of No Time for Slaves, proposed a simple formula to facilitate understanding of the interplay between government and economics: government + religion = economics. According to Hanke, the problem with Venezuela and its hyperinflation is Hugo Chavez's successor, Maduro; the problem in Yugoslavia was Milosevic; the problem in Zimbabwe was and is Mugabe. They all adhered to the ten-point playbook of the Communist Manifesto, which wrecked their economies and the social order. According to McMaster government does not operate in a vacuum, but those who lead administer by their philosophy or religion.

This simple, but profound theorem plays out around the world today. It can lead to prosperity or economic crisis and hyperinflation. In America, this theorem has led to prosperity. The respect for individual rights and property rights are the pillars of the free market. The founders assured these rights through the founding documents, especially the U.S. Constitution.

According to Coltart (see Part One), the primary reason for Zimbabwe's hyperinflation was that the deficiencies of their constitution allowed a vast disparity of power between the executive office and the legislative and judicial branches. Most worrisome relative to the U.S. Constitution are a list of Supreme Court reversed Executive Orders that even liberal law scholars say blatantly violate the Constitution. It is the quality, not the quantity (above ) of these orders that is the issue. If Americans continue to allow this executive tendency to span administrations, as they have in the past, the dilution of their constitutional rights may eventually lead to hyperinflation in the U.S.A.

For the present, inflation and money velocity remain low. Though there are various reasons high inflation may appear, typically, there need to be two elements: economic capacity, including low unemployment, and high money velocity. With even core inflation (PCE) currently under 1.2% (as of June 15th headline PCE is 0.2%), economic capacity and lower unemployment just emerging, and money velocity still quite low, high inflation does not appear to be on the horizon.

This is not to say that other factors could not instigate high inflation or hyperinflation. Some of these "black swans" are dealt with below. But, while Reinhart and Rogoff are no doubt right about the rampant denial afflicting advanced nations relative to future sub-par growth, QE, debt restructuring and coming high inflation, a crisis appears years away. Greece is symbolic of that looming crisis; but it is not Bear Stearns or Lehman.

This time is not different; but global reserve status, the trust and confidence of investors and deep and wide financial markets make the U.S. unique. There are still enough questions not to be dogmatic, but until the U.S. experiences an increase in causal symptoms or a black swan that fractures global confidence in its economy, hyperinflation is not a worry.

Black swans that could lead to high inflation or hyperinflation

The above being noted, according to FT, the global system is in many ways more fragile today than before the GFC. And, considering its fragile nature, many incidents could come out of nowhere and lead to a crisis, or series of crises, that eventually results in a currency crisis and/or hyperinflation.

One of the prominent possibilities is a successful cyber-attack on a major institution or the U.S. itself, especially the nation's power grids, its nuclear plants, its water supply or its major financial institutions. JPM's, NASDAQ's, and Sony's recent experience serve as examples, and with increasing tensions with Russia and China this area will continue to be a challenge. The director of the NSA recently warned that a cyber-attack will cause a major systems collapse within a decade unless the U.S. develops counter strategy immediately. According to Greg Medcraft, chairman of the board of the International Organization of Securities Commissions, the next black swan will be a cyber-attack.

Though the U.S. has largely avoided catastrophe in the past, there is also the possibility that it might experience more natural disasters in the future. Remember Zimbabwe? About 19% of the U.S. is presently in severe or extreme drought, 29% in moderate to extreme conditions and approximately 40% in abnormal dryness or greater. 100% of California is in extreme, severe or exceptional drought. Also alarming is that according to the Wall Street Journal U.S. beekeepers have been losing 30% of their bees for the last decade, above the 19% sustainable rate. The above issues may place strains on agriculture, lead to supply disruptions and drive up food prices in future years.

As I covered more extensively in “Evaluating the Arguments for the Dollar's Demise,” in the last decade, globally, at least, there has been an, apparent, increase in natural disasters. According to a 2013 article in The New England Journal of Medicine, there were three times as many natural disasters from 2000 to 2009 as there were from 1980 to 1989. And, according to one account, it was the 1906 San Francisco earthquake and fire that led directly to the Financial Panic of 1907.

In another critical area, both George W. Bush and Barack Obama have identified nuclear terrorism as the greatest threat to national security. According to a 2008 FBI study, any terrorist nuclear weapon is likely to have a yield of about 1-kiloton (chart, below ), large enough to destroy a city center and with the potential to contaminate surrounding area for up to 4 miles, depending on wind direction (chart, 2nd below ). According to Nukemap, a 1-kiloton detonation in lower Manhattan would kill about 30,000 people and cause three times as many injuries, some fatal. A smaller possibility is a 10-kiloton event with fallout reaching 20 miles.

Even before 911, the U.S. recognized that terrorist groups were attempting to acquire nuclear material. According to one recent joint report by Belfer Center at Harvard endorsed by military leaders, constructing a crude nuclear device is easier today than constructing a safe, reliable weapon. Tests indicate that intelligent operatives could defeat security systems holding weapons or materials and in the last five years several sites have been penetrated. As of 2014, at least four key core Al Qaeda nuclear operatives were still at large. And the difficulty of smuggling nuclear material into the U.S. is largely overstated. But the primary concern is that with one detonation terrorists could claim they had more bombs hidden, creating mass panic.

The nuclear scenario would be a global catastrophe, claiming thousands of lives, shutting down trade and exporting dire consequences to other nations. The cost in response and retaliation would also add enormously to U.S. debt, potentially accelerating the nation towards economic crisis. According to the above Belfer report, the risk of a nuclear terrorist attack on U.S. soil is greater than 1 in 100 every single year.

In addition to all of the above possibilities there are ongoing currency wars, the reemergence of the Eurozone crisis, the Ukraine and the potential destabilization of Russia, the China slowdown and real estate bubble, Japanese debt, the Sino-Japanese conflict and the craziness of mad regimes like North Korea and Iran to worry about. And we haven't even addressed nuclear sabotage, dirty bombs, an EMP device, ISIS and the Middle East as a whole, other U.S. terrorist events, central bank errors or another financial meltdown due to the approximately $70 trillion in global derivatives. In many ways, the world we currently live in is like dry kindling waiting for an inerrant spark to set it ablaze.

Hyperinflation in the U.S.A.: How and when it might happen

The risk of the economy collapsing and instigating hyperinflation is much like the theory of the avalanche: many of the items are in place, and all that is needed is the right trigger to set them off. Whether it comes in the next few years or twenty years from now is impossible to predict and depends on too many unknowns.

Some, like Eswar S. Prasad, argue in The Dollar Trap that the intricate nature of global mechanisms will keep the dollar in play indefinitely – and the world largely in balance. Others, like James Rickards, in The Death of Money, insist that the complexity of global financial interactions and their tipping points will crash the U.S. economic system. Who is right?

Based on the above analysis, unless the U.S. experiences a crisis greater than 911 or the GFC, hyperinflation is not a likely scenario for the next five years and probably more like twenty years. But, the greater and the more numerous crises are, the more likely that hyperinflation will come quickly. What if a black swan or a series of crises led to a perfect storm?

A 1 kiloton nuclear terrorist attack strikes the U.S. in either New York City or Washington D.C. The stock markets crash, losing half their value. The EZ breaks apart and the resulting malaise spreads to the global economy. Instead of the confidence in crisis coming to the U.S., the U.S. bond market implodes and global money runs to gold, silver, foreign currencies and various ex-US bonds. In the U.S. prices rise and stocks rebound some with them – eventually. The U.S. military retaliates in foreign lands for the nuclear attack but walks into a trap.

Disunity disintegrates into political civil war and panic incites unrest, resulting in martial law. The current drought increases and food supply is cut in half. Fed printing presses finally result in high inflation. Destruction from an earthquake and/or a volcanic eruption lays waste to much of a major city. All of these events combined destroy infrastructure, disrupt distribution, exacerbate the drought and kill leaders. Foreign governments take advantage of America's weakness and institute a cyber-attack. Power failures occur nation-wide.

Hyperinflation ensues. The stock market falls as confidence wanes. Loss of control leads to a government coup, bank account freezes and despotism. The U.S. descends into an inflationary depression leading to fear of invasion, the dollar's fall and its replacement as the global reserve.

It would probably take more than one isolated event – even a major one – to create the conditions for hyperinflation in the U.S. And, it took a decade for a similar process to unfold in other nations. But, it can occur faster in the midst of critical events.

As I stated in “Evaluating the Arguments for the Dollar's Demise,” the U.S. has been protected by a hedge when it comes to disaster. But, events like Katrina, national drought, and the recent Supreme Court decisions relative to Constitutional interpretation hint at a new and more divisive era. Though for the present things seem fine, there is more than one route to an avalanche now than there may have been just a few years ago.

Replacement of the dollar as global reserve as an isolated event might instigate hyperinflation more quickly. However, only one reserve currency nation has ever experienced a hyperinflation – France, from 1795-96, during the years of the French Revolution. And no nation has ever experienced a hyperinflation as a result of losing global reserve status. Other causal symptoms would likely be apparent, leaving some time to prepare.

How to prepare for hyperinflation

Here is some broad investment advice that takes into account the dichotomy of the above conclusions relative to hyperinflation. Portfolio allocations can start small and increase as events on the ground change:

-

Protect what you have: Diversify your portfolio globally. Hold some real estate. Borrow at fixed rates while interest rates are low.

-

Consider an international account. Set up expeditious portfolio transitions into foreign currency accounts and international funds with a flexible strategy for transference of at least some assets in the event of escalating volatility, major U.S. weakness or black swans.

-

Allocate part of your portfolio to alternative funds and hedge-fund-like strategies. If qualified, consider hedge funds, especially those with a global macro and/or event-driven focus.

![Silver and gold in marks]()

-

Consider natural resources, agriculture and commodities based funds, especially now when commodities overall, including oil, have corrected and mining is near a historical low cost point versus gold. Remember that water is liquid gold and may be scarcer in the future.

-

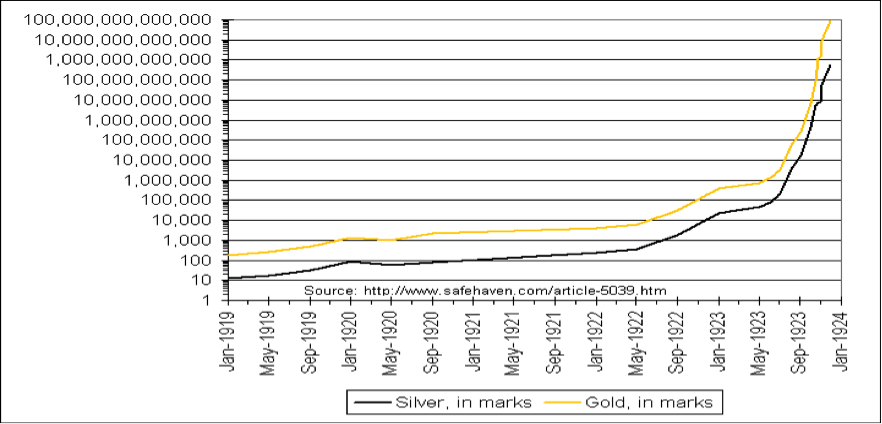

Accumulate tradable items: physical gold and silver (the chart above shows the rise of gold and silver during the Weimar Germany hyperinflation); jewelry; stored food and water; wine; and foreign currency.

Hyperinflation in the U.S. is coming sometime in the next 20 years or so, and this isn't a cry from a Chicken Little, but a conclusion that the analysis strongly suggests. It is possible hyperinflation could happen during the next few years, but that seems unlikely since it would require a series of major crises and political blunders – events unprecedented in the history of the United States. If this led to a corruption of Constitutional rights in the midst of an exaltation of the Executive Branch that resulted in loss of the rule of law, hyperinflation might result. This is why the understanding and interpretation of the U.S. Constitution, especially in the context of executive orders, may be the most important issue before Congress, the judicial branch and the American people over the next few years – regardless of which party rules.

It is much more probable that hyperinflation, when it comes to the U.S., will be preceded by a long slow decline that will include a protracted period of high inflation, and that the crash of the dollar and hyperinflation will be the final tumble off a looming, steep cliff. The indications from this analysis point to a convergence of events sometime in the mid-2020's to early 2030's – unless the American people can somehow unite and motivate their politicians to accomplish the hard, almost impossible task of cutting mountainous entitlements adding annually to U.S. debt. But, of course, if the perfect storm occurs, hyperinflation could arrive sooner.

For the chaos of change it brings, hyperinflation has been described as an economy without memory. It can also be viewed as a furtive civil war a nation's political leaders wage with its people over who will pay for the nation's sins. Its battlegrounds, victories and defeats answer the question of who will wave the white flag over the extravagance of the nation's mismanagement. Ultimately, the people – and the leaders – are both forced to surrender.

The good news is that, with time, every nation returns from the devastation of hyperinflation to the degree that it embraces corrective measures and free market principles. Regardless of what else might occur, in this sense the U.S. has a sure foundation, a rich history and a hopeful future.